[ad_1]

Gerasimov174

Introduction

I wasn’t planning on writing this article, to be honest. I’ve ranted a lot about failing energy policies, the European energy crisis, the return to coal, and related topics. However, the market wanted me to add to my Devon Energy (NYSE:DVN) position. In this article, I will share my views on the energy market from a political and macro point of view and explain why Devon Energy is a fantastic tool for investors who want to benefit from a (potentially) very high cash flow instead of an oil company that aggressively buys back its shares. If you’re into that, you’ll like my Marathon Oil (MRO) article, which you can access here.

Devon Energy is the best tool for income-oriented investors in a market seeing severe supply shortages, politicians unwilling to make changes, and a market that is providing new entry opportunities after the latest demand-fear sell-off.

It’s shaping up to be a new era of oil gains and income.

Now, let’s look at the details!

All About SUPPLY

I would get really sick of talking about oil supply if it weren’t such an important and fascinating topic.

For the first time in decades, we’re in a situation where all eyes are on supply instead of demand (which is important as well).

In the most recent two oil crashes (2014/2015) and 2020, oil supply was a major issue.

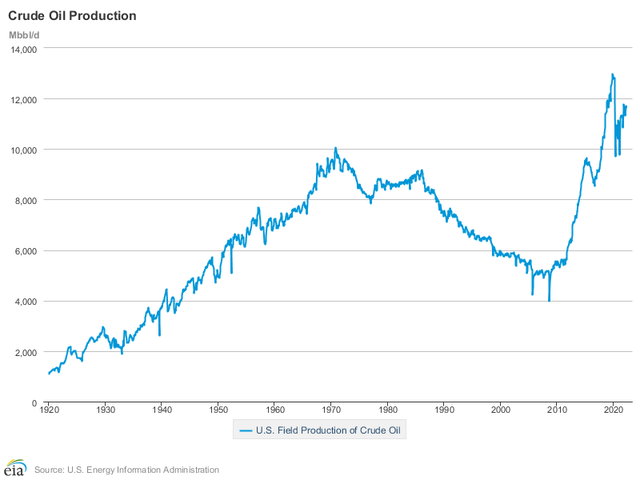

The start of the shale revolution after the Great Financial Crisis allowed the US to boost crude oil production from roughly 5 million barrels per day to currently 11.6 million barrels per day. This is as of April 22, the most recent data according to the US Energy Information Administration.

EIA

That’s fantastic news for US energy security, but it was somewhat bad news for the drillers who made this production upswing possible. After all, it caused supply to rise so much that oil crashed two times when demand faded (2014/2015) and 2020. After 2014/2015, oil companies quickly boosted output in order to repair their balance sheets – the manufacturing and commodity recession had done a lot of damage. This once again resulted in an even higher supply. This surge in supply and the fact that 2020 lockdowns caused demand to implode briefly pushed (front month) WTI crude oil prices into negative territory in 2020.

Then, something changed. Production didn’t rise anymore.

Production is now roughly where it was one year ago and well below peak levels close to 13 million barrels per day.

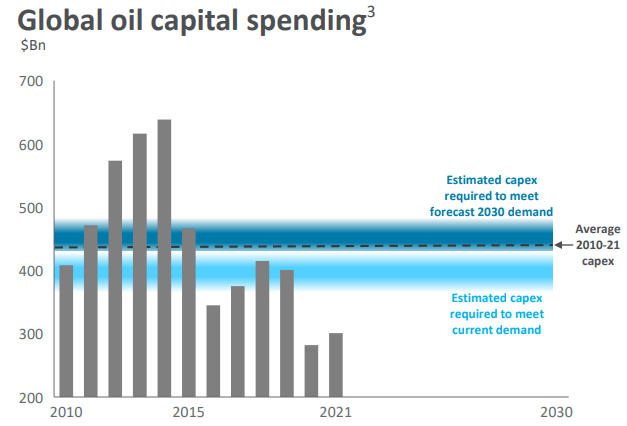

As the chart below shows, global oil capital expenditures have gradually been reduced. Prior to the 2014 oil crash (when Venezuela was still a rich country), global oil CapEx was close to $650 billion. This imploded when a lot of offshore projects became unprofitable. The surge in CapEx between 2016 and 2018 was mainly caused by US onshore drillers. Then, the pandemic caused another major decline to less than $300 billion. This is now expected to remain the base case. Needless to say, the global hunger for oil remains high and further rising. In order to satisfy 2030 demand, global oil CapEx is estimated to require at least $450 billion annually.

Seeking Alpha

The unwillingness to invest in growth is based on a number of reasons. However, the biggest reason is the global transition to renewable energy. The Paris Agreement and various initiatives to become carbon neutral have made oil and gas companies the “bad guys”.

As discussed in my recent Marathon Oil article, major politicians are coming out, making the case that everything is going according to plan.

The other day, I read the following headline:

New York Post

The New York Post – among many others – reported that National Economic Council director Brian Deese (Biden’s personal advisor) had a somewhat unexpected answer to the following question asked by CNN:

“What do you say to those families who say, ‘Listen, we can’t afford to pay $4.85 a gallon for months, if not years. This is just not sustainable’?”

He answered:

“What you heard from the president today was a clear articulation of the stakes,” Deese answered. “This is about the future of the liberal world order and we have to stand firm.”

These signs are everywhere. In the Netherlands, boosting production in one of the world’s largest gas fields is controversial and production is expected to end in 2023. Bear in mind that Europe is in a major energy crisis right now.

Bloomberg

Or this:

The Globe And Mail

In the UK, Lord David Frost wrote an article in The Telegraph titled “Energy rationing is inevitable without a fundamental rethink of net-zero”, where he looked at the current situation from a United Kingdom point of view. It’s similar as the government has reduced permits for offshore oil production while boosting renewables in a time when energy supply has become a huge issue.

So what is to be done? The Government must realise that it faces a crisis. In the short run it must keep the lights on or pay a heavy price. It should then drop the mad dash for medieval wind power technology and focus on the only acceptably low-carbon form of power available – gas. Get shale gas extraction going, commit long-term to the North Sea, put in place proper storage – and build some new gas power stations. By all means commit to nuclear, too – but only gas solves the problems in a meaningful time frame.

Of course I don’t think this will happen. We will muddle along, and then, one day soon, when we realise we don’t have the energy our economy needs, whoever is in power then will resort to rationing.

With that said, in a recent interview with Dubai-based Asharq TV (no link available while I’m writing this), I said that the latest slump in oil prices was caused by demand fears given that investors started to price in a recession. While I have zero doubt that oil will remain very volatile, the supply side is broken, which will prevent oil from crashing as it used to in prior cycles.

And it’s not just the US, it’s all major oil producers as Goehring & Rozencwajg write:

Years of underinvestment in upstream oil and gas projects has produced the present deficit. Trying to reverse this shortfall will take years of upstream capital spending at rates double and triple of what we are spending today. Until we reverse this shortfall in upstream capital spending, we will not fix the underlying problem.

Goehring & Rozencwajg

Moreover, they highlight a very important aspect related to renewables, which I need to include as well:

Oil and gas capital spending fell by over 60% between 2010 and 2020. Investment in the US shales fell by over 70%. Over that entire period, the cumulative reduction in capital spending compared to trend was more than $1 tr.

Over the same period, ESG concerns came to grip the global investor community. We believe much of the capital needed to build renewable projects was diverted away from upstream oil and gas investment. Unfortunately, wind and solar are intermittent sources of power that suffer from very poor energy efficiency.

With that said, I’m rooting for renewables – especially nuclear energy. It is extremely important that the world has (clean) affordable and reliable energy. However, the transition needs to be much slower. It is absolutely impossible to force a trend towards renewables without breaking supply chains. Hence, my oil and coal-focused articles aren’t part of a vendetta against renewables but an honest concern of mine that we’re going in the wrong direction. As part of my job, I am swamped with stories every day that show how bad things have gotten in energy – especially in Europe.

For example, using the United States as an example, 79% of total energy comes from fossil fuels. Not only does switching this to renewables take a lot of time, but creating inflation in these areas works its way through the entire economy, causing the situation we’re in now.

EIA

In 2020 and early 2021, central banks made clear that creating sustainable inflation close to 2% was important. Hence they stimulated economies and commented that inflation fears were overblown. I saw it as a sign that they wanted us to buy inflation trades.

Now, I get the same feeling from politicians in this energy crisis when it comes to oil stocks. Comments like the creation of a new Liberal World Order are the ultimate reason for me to buy more oil.

It is almost certain that we remain in a situation where companies continue to focus on free cash flow as the downside is simply too high. Why focus on production growth? For most (smaller) drillers, it’s not certain they will get the capital needed to survive during the next potential downturn.

With that said, here’s why I like Devon Energy.

Devon – Income & Capital Gains

Devon and Marathon Oil have been on my radar for years. Now, both are great complementary investments. While Marathon spends most of its cash on buybacks, Devon Energy has become a high-yield play thanks to its emphasis on dividends.

With a market cap of $33.7 billion, Devon Energy is one of America’s largest onshore oil drillers.

In 1Q22, the company produced 288 thousand barrels of oil per day. 209 thousand barrels came from the Delaware Basin. 32K barrels were produced in the Williston Basin followed by Eagle Ford (17K). The company also produced 136 thousand barrels of natural gas liquids. 92K barrels came from the Delaware Basin. Total gas production was 906 MMcf per day. 561 MMcf per day came from the Delaware Basin.

On top of that, the company bought the leasehold interest and related assets of RimRock Oil and Gas LP, a Warburg Pincus portfolio company, for $865 million on June 8.

As a result, the total 1Q22 production was 575 MBOED (thousand barrels of oil equivalent per day). 50% of this volume came from crude oil, making Devon a large natural gas player as well.

That’s important as I see a strong long-term bull case for natural gas as well as explained in this article.

Devon Energy aims to hike production by 5% annually, which is conservative. 20% of volumes are hedged for 2022, which means the company does benefit from the upside in oil instead of losing money on hedges.

For example, in 1Q22, the average oil price was $94.45 per barrel WTI. DVN realized $92.9 per barrel (pre-hedges). After hedges, the company ended up with a realized price of $81.6. That’s more than decent.

Moreover, the company is breakeven at $30 WTI and $2.50 Henry Hub, which is fantastic news for free cash flow at high oil prices.

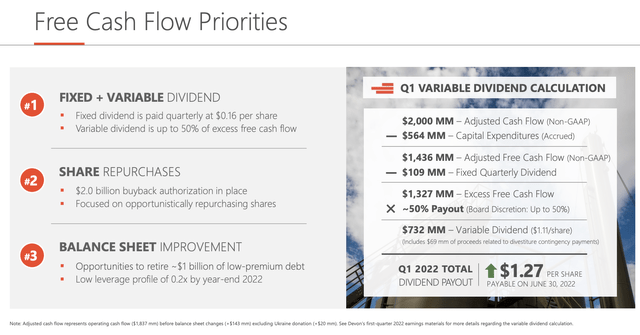

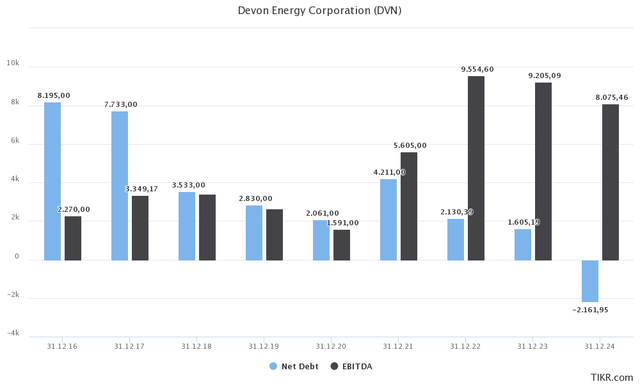

Speaking of free cash flow, the company’s number one priority is its dividend. A lot of peers prefer balance sheet health, but that’s not key here as the company is on pace to lower its leverage ratio to 0.2x by the end of this year (down from 1.4x on 3/31/2021).

Devon Energy

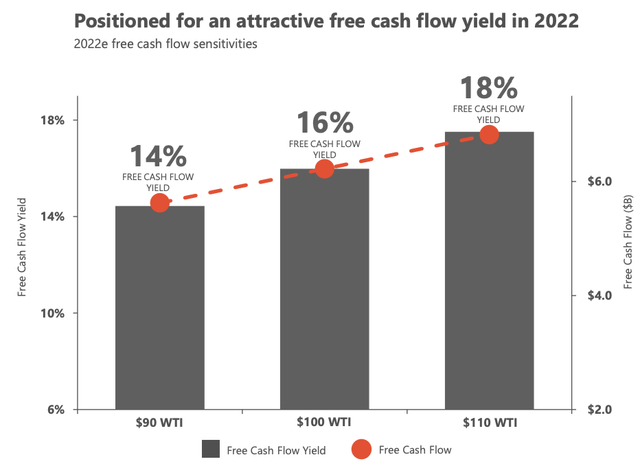

In the case of Devon, the company needs roughly $1.9 to $2.2 billion in capital for its upstream operations (production). This – and its low breakeven prices – indicates a high implied free cash flow yield at high oil prices. At $90 WTI, Devon estimates that its free cash flow yield is 14%. This is based on its April 29, 2022 market share. Back then, the company’s market cap was $38.4 billion. It’s $33.7 billion now resulting in an implied FCF yield of 16% at $90 WTI.

Devon Energy

This number is 18.2% at $100 WTI and 21% at $110 WTI. That’s mighty impressive and the basis for a double-digit dividend yield if oil remains above $100.

Note that this dividend consists of a (low) fixed dividend and a variable dividend consisting of 50% of excess free cash flow.

The excess cash flow after that (excess-excess cash flow?) is spent on buybacks. As of 1Q22, the company has a buyback authorization of $2.0 billion. So far, $891 million worth of shares has officially been bought back. That number will be far higher when the company reports 2Q22 earnings.

The program aims to buy back 5% of shares outstanding, which is a great bonus on top of dividends.

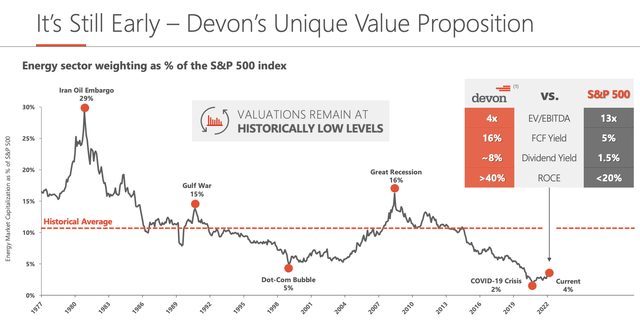

Valuation

If oil remains above $100 on a longer-term basis, Devon is too cheap. An implied free cash flow yield of 18% at these oil prices is ridiculous. Sooner or later, the market will recognize this quality and continue to shift money to oil and gas companies like Devon.

Devon Energy

Using the company’s $33.7 billion market cap, $1.6 billion in expected 2023 net debt, $140 million in minority interest, and $9.2 billion in expected EBITDA, we’re dealing with an enterprise value of $35.4 billion, or 3.9x expected EBITDA.

TIKR.com

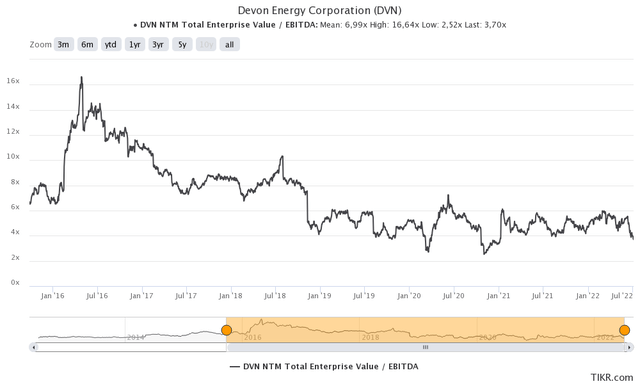

That’s too cheap and I would make the case that 5.0x NTM EBITDA is more appropriate, which implies a $44.3 billion market cap (at least 33% upside in a conservative scenario).

TIKR.com

*If* we’re indeed in a long-term commodity upswing, I think DVN easily doubles over the next 2 years. Maybe faster depending on how the economy deals with high inflation.

Takeaway

In this article, I wanted to achieve two things.

First, to explain my view on energy commodities based on significant supply issues that are unlikely to be solved soon as years of underinvestment will need years of accelerating CapEx to boost production. On top of that, we’re dealing with politicians who celebrate high energy costs as it fuels their desire to boost renewable energy (and related).

That doesn’t sit right with me.

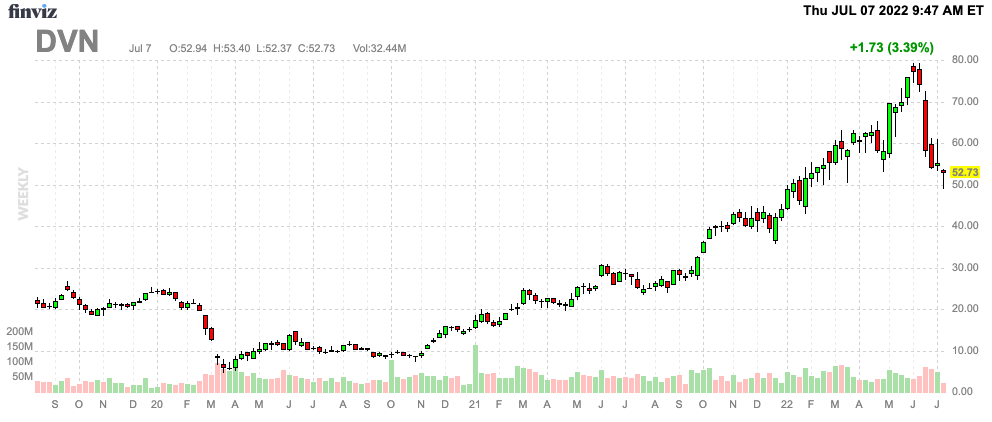

However, it’s almost a guarantee that the oil supply will remain subdued, opening up fantastic opportunities in that area. I recently added DVN shares to my portfolio (at $50.77 on July 6) because Devon has both oil and gas exposure, a very low breakeven price, an emphasis on dividends, and a valuation that makes too much sense to ignore.

I believe the risk/reward is terrific and I don’t expect to sell DVN shares at a profit of less than 35% this year.

However, and this is very important, please be aware that oil is very cyclical and volatile. As good as these bull cases may sound, do not go overweight oil but focus on a well-diversified long-term portfolio. Oil can do a lot of damage during downturns (the most recent downtrend is a good example).

FINVIZ

So, please keep that in mind.

(Dis)agree? Let me know in the comments!

[ad_2]

Source link

More Stories

The Best Sugar Scrub Essential Oils with Aromatherapy Benefits

Sezane – A Guide to their Summer Editions Collection

Beyond the Basics: Advanced Techniques for Successful Marketing Planning in the Banking Industry